Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

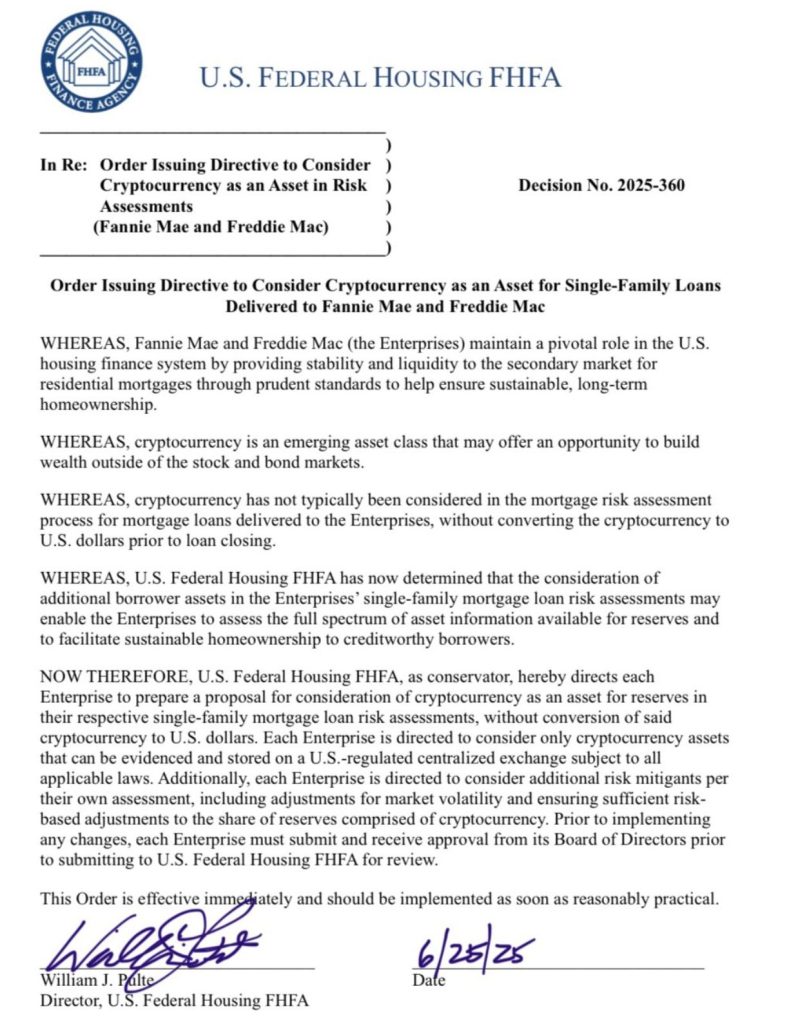

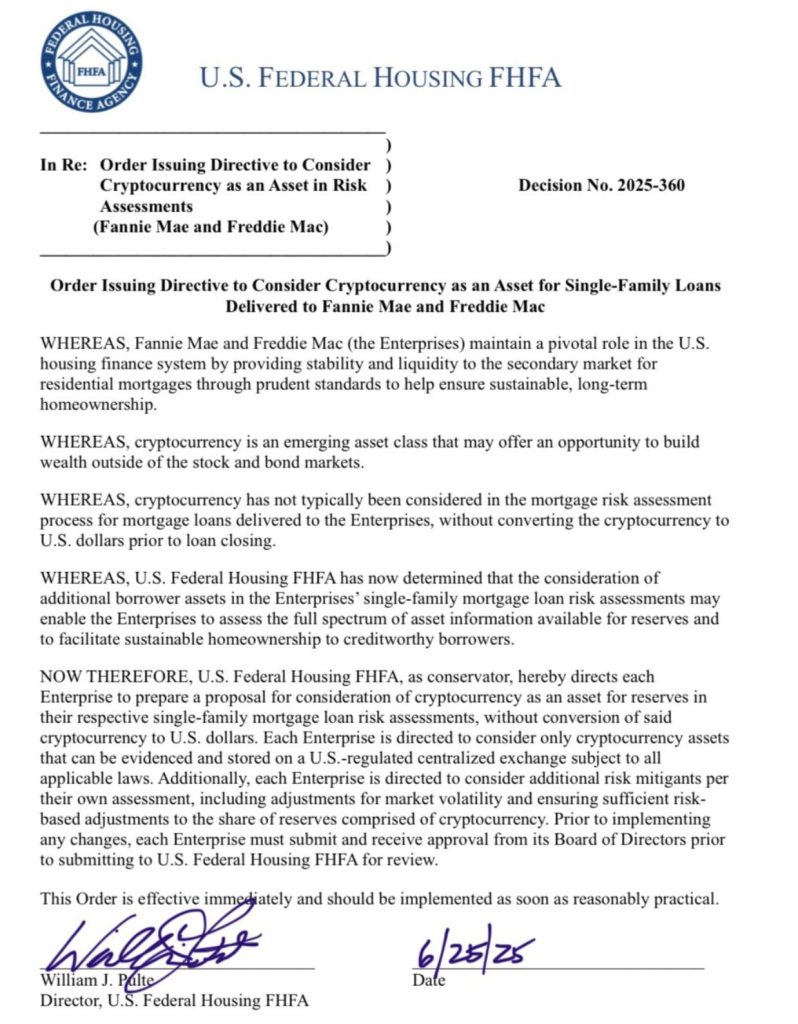

In an extraordinary shift in the US Federal Housing Financing Agency Debtors may soon use crypto investment to qualify for mortgages.

Michael Saylor It could hardly contain its joy when the order details appeared – to describe it as a “defining moment for recognition of collateral”.

Then again it is quite surprising because it was sufficiently reckless to suggested to consume consumers to take mortgages to invest in Bitcoin.

The plans were submitted by FHFA director Bill Pulte, who himself is an essential investor in digital assets. Sharing a proposal on X, wrote:

“After a significant study and in accordance with President Trump’s vision to become a crypt of the world in the world, I ordered great Fannie Mae and Freddie Mac today to prepare their businesses to count the cryptocurrency as an asset of mortgages.”

At the moment, however, it is worth taking a huge step back – and given the possible consequences that this policy could have on homeowners and economics.

We all know how volatile bitcoins can be. It’s accelerated from $ 61,000 to $ 107,000 over the past 12 months. Such dramatic price movements also work in both ways, with a devastating decline from $ 68,000 to $ 16,000 back in 2022.

Acceptance of BTC as a collateral would mean that enthusiasts no longer have to transfer their coins back to dollars, but can keep them in the hope of future prices. On the other hand, there is a real risk that the crypto of the house owner can be destroyed in the event of a sudden decline. In other words, it would mean slavely to monitor prices to avoid a devastating margin.

Digital assets are also a quite impractical source of funding for the purchase of house. When using Fiat, applicants may need only 5% to 10% cash deposit – which means that they can borrow the rest and perform monthly installments. On the other hand, most crypt mortgage providers require 100% collateralization. In other words, if you have your heart set up to a $ 300,000 house, you must commit $ 300,000 coins. It is also worth mentioning that creditors usually accept only BTC and Ethwhich means that your DOGE Bags wouldn’t get you too far in the application process.

Critics already share concerns that Krypto injections to the housing market could contribute to the financial crisis of a similar year in 2008, where it has not come true and caused a global recession of a high -risk mortgage. Since the US government implicitly guarantees housing loans issued by Fannia and Freddie Mac, there is also a real danger that a bitcoin impliance could end the costs of taxpayers.

In order to balance it is important to recognize the points of pain that crypto investors currently face when trying to get on the real estate ladder – a considerable challenge, because real estate prices will be controlled by control.

For one, creditors in some countries penalize Applicants if transactions include cryptocurrencies will appear on their statements. This is grossly unfair and outdated thinking that urgently has to change.

Many banks are also incredibly inflexible when considering revenue sources-especially when it comes to self-employed. Someone who works as a single $ 100,000 income dealer could eventually be able to borrow significantly less than a full -time employee with the same salary.

A few years ago, Redin’s data also revealed that about 12% of buyers first sold crypto to finance their advances. Given how the value of bitcoins has increased significantly since then, it means that they missed a significant amount of profit.

Josip Rupen, CEO Mortgage Milo, recently said Mortgage for professional America:

“There are many clients who have accumulated bitcoin wealth more than 10 years ago, when bitcoins traded for $ 100. Now trading with bitcoins is $ 85,000. It has become a significant part of their net assets and do not want to sell it.”

It is unacceptable for crypto investors for creditors to treat as Pariahs. Everyone needs a home. However, these instructions submitted by FHFA actually have the potential endanger These bitcoins holders and threaten the economy by binding the fates of digital assets and traditional finances.

Bitcoin now looks pink now – and pushes $ 108,000. But what happens on the next bear market when there is a real chance of an 80% accident and what would it mean for homeowners who have a roof over their heads because of their crypt?

Responding to responsibility: Opinions in this article are their own writer and do not necessarily present opinions on kryptonews.com. The purpose of this article is to provide a wide view of its topic and should not be considered a professional advice.

Contribution Opinion: Mixing crypto and mortgages is a recipe for disaster He appeared for the first time Cryptonews.